Purchasing an individual life insurance policy is one of the most practical steps an income earner can take to protect their family financial future. For decades, you pay steady monthly premiums to lock in a protective safety net. In return, the insurance provider promises to deliver a substantial capital payout to your loved ones if you pass away while the policy remains active.

However, many policyholders and beneficiaries do not fully understand what happens after the policy is put in place. How exactly do your loved ones transition from holding a contract document to receiving the actual financial payout? What obstacles can cause an administrative delay, and how do changing industry regulations impact processing speed?

The current economic landscape makes a smooth claims process more vital than ever. Driven by persistent cost of living adjustments, elevated core consumer prices, and shifting regulatory frameworks across states, the financial pressure on grieving households has increased significantly. Recent report findings indicate that insurance companies have upgraded their administrative tracking software. This means that while payouts can be resolved faster than ever, any filing errors or incomplete documentation can instantly halt the process. Let’s look at the operational mechanics of life insurance payouts, map out the step by step claims framework, and establish a clear timeline blueprint to ensure your family is protected when they need it most.

The Core Concept: Direct Contractual Wealth Transfer

To understand how life insurance payouts operate, you must recognize that a life insurance policy is a legally binding private contract. Unlike real estate, physical vehicles, or personal belongings, a life insurance payout bypasses the traditional probate court process.

When an individual passes away with a valid individual life insurance contract, the death benefit is transferred directly to the designated beneficiaries. This direct transfer means the money is completely shielded from probate attorneys, estate executors, and civil creditors. The capital is paid out directly, providing immediate liquid assets to help the household manage urgent liabilities without waiting months for court systems to settle the estate.

Structural Comparison: Payout Distribution Formats

When filing a claim, beneficiaries are typically offered a choice between several payout distribution formats. Selecting the right structure depends entirely on your family’s long term financial objectives and current cash flow needs.

Distribution Strategy

Core Operational Mechanism

Primary Financial Benefit

Ideal Household Profile

Lump-Sum Payment

The entire face value of the policy is distributed as a single tax free check or electronic fund transfer.

Provides immediate, unrestricted liquidity to clear major debts or mortgages.

Families carrying large fixed liabilities or immediate mortgage principals.

Specific Income Installments

The total death benefit is placed into an interest bearing account and paid out via structured monthly payments.

Guarantees a predictable, multi year cash flow to replace a steady income.

Surviving spouses managing ongoing living expenses and childcare logistics.

Life Income Annuity Track

The carrier converts the payout into a guaranteed lifetime annuity stream based on the beneficiary’s age.

Eliminates the risk of outliving your capital by guaranteeing lifetime payments.

The insurance company places the payout into a dedicated checkbook account, earning basic interest.

Offers a flexible stopgap, allowing you to access cash while planning long term investments.

Beneficiaries who need time to consult with professional wealth managers.

Step-by-Step Claims Execution Framework

A life insurance payout does not happen automatically. Insurance companies do not track public vital statistics records in real time to trigger payouts. The designated beneficiaries must actively initiate the claim by completing a structured four step process.

Step 1: Secure Certified Documentation

The claims process begins by gathering required verification documents. Beneficiaries must secure the original policy number details and obtain multiple certified copies of the official death certificate from the local vital statistics office or funeral director. Most insurance carriers require a certified death certificate featuring a raised official seal before they can process a file.

Step 2: Submit the Official Claimant Statement

Each designated beneficiary must fill out an independent claimant statement form provided by the insurance company. This document verifies your identity, confirms your current contact information, and establishes your preferred capital distribution structure (such as a lump sum electronic bank transfer or a structured monthly annuity).

Step 3: The Carrier Contract Review

Once the paperwork is submitted, the insurance provider’s claims department opens an administrative audit. Underwriters verify that the policy was fully active at the time of passing, confirm that all monthly premium balances were paid up to date, and check if the claim falls within any standard contractual exclusion windows, such as the two year contestability period.

Step 4: Final Fund Settlement

After validating the documentation, the insurance company releases the funds. The capital shifts out of the company reserves directly into the beneficiary’s active banking accounts, completing the direct transfer of wealth.

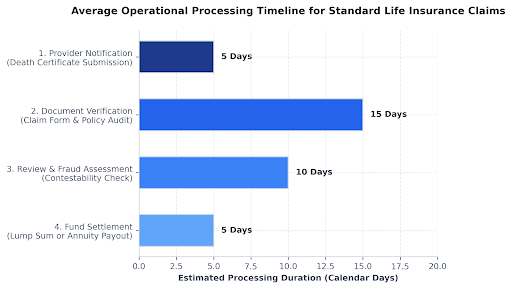

Visualizing the Processing Timeline

To understand how long this administrative process takes, you must look at the standard operational timeline of modern insurance carriers. The following chart illustrates the average processing duration for a standard, undisputed life insurance claim from initial notification through final fund settlement.

Understanding Potential Processing Delays

While standard, undisputed life insurance claims are typically resolved within 30 days, specific variables can extend the administrative processing window significantly. Beneficiaries must prepare for two primary potential hurdles:

1. The Two-Year Contestability Clause

Every standard life insurance contract contains a built-in consumer protection clause called the Contestability Period, which lasts for the first two years from the policy’s effective start date. If the insured individual passes away within this two year window, the insurance carrier is legally required to conduct an expanded background audit before paying the claim.

During a contestability audit, underwriters request and review complete electronic health records, past lab test results, and medical billing logs. The goal is to verify that the original application data matches the historical medical reality.

If the insurer uncovers material misrepresentations on the initial application, such as hiding a chronic type 2 diabetes diagnosis or omitting a tobacco user status, they have the right to deny the claim entirely, refunding only the paid premiums to the beneficiaries. If the policy has been active for more than two years, it becomes contractually incontestable, meaning the carrier must pay the claim regardless of application omissions, except in rare cases of outright premium fraud.

2. Complex Homicide or Accidental Verification Loops

If a death certificate lists the cause of passing as a homicide, accident, or undetermined event, the insurance carrier cannot rely solely on standard medical records. They must open an active verification loop with local law enforcement agencies and medical examiners to rule out specific policy exclusions, such as the beneficiary’s direct involvement in the event. This inter agency coordination can extend the processing timeline by months or even years while the official investigation concludes.

Tax Realities: Are Life Insurance Payouts Taxable?

One of the most valuable aspects of individual life insurance planning is its highly favorable treatment under federal tax codes. According to current IRS regulations, life insurance death benefits are completely exempt from federal income taxes.

Whether your beneficiaries receive a $250,000 policy payout or a multi million dollar settlement, they do not have to report the lump sum as taxable gross income. They receive the full face value of the policy without any deductions for federal or state income taxes.

Essential Nuances to Keep in Mind

Accumulated Interest Income Is Taxable: If a beneficiary chooses a structured installation track or a retained asset account, the principal death benefit remains entirely tax free. However, any additional interest income generated by the carrier while holding those funds is subject to standard income tax reporting rules.

Estate Tax Threshold Considerations: If a policyholder owns their life insurance policy directly at the time of their passing, the total value of the death benefit is included in their gross taxable estate. For high net worth individuals, this can potentially trigger federal or state estate taxes. To avoid this exposure, affluent families often use an Irrevocable Life Insurance Trust (ILIT) to own the policy, moving the death benefit entirely outside their taxable personal estate.

Step-by-Step Planning Checklist for Families

To protect your family from administrative friction and ensure a smooth claims process, use this proactive strategy to organize your portfolio:

Step 1: Consolidate Policy Information in a Secure Location

Store your original life insurance contract files, policy numbers, insurance company contact information, and local broker records in a centralized, highly secure digital folder or home fireproof safe. Ensure your designated beneficiaries know exactly where these files are located and how to access them.

Step 2: Perform Regular Reviews of Beneficiary Designations

Your household configuration is not static. Significant life events like marriages, divorces, births, or wealth shifts should prompt a review of your policy parameters. Reviewing your designations every three to five years ensures your protection remains aligned with your family’s actual dynamics, preventing capital from being inadvertently routed to an ex spouse or tied up in probate court because a beneficiary designation is outdated.

Claims Timeline & Readiness Audit

Assess your administrative paperwork status to calculate an expected fund settlement window and identify potential carrier delay vectors.

1. Case Parameters & Checklist

Policies active under 2 years are legally subject to standard contestability verification.

2. Processing Diagnostics

Administrative Readiness Score

0/100

Projected Settlement Timeline

Select parameters…

Strategic Advisory Brief

Awaiting asset audit inputs…

Step 3: Work with an Independent Advisor

If you are managing a substantial insurance portfolio or establishing long term inheritance plans, consult with an independent insurance broker or estate planning attorney. Independent specialists can evaluate your household’s liabilities anonymously across major carriers, helping you structure your policy ownership and beneficiary designations to minimize tax exposure and keep your family fully protected.

Summary and Next Steps

An individual life insurance policy is a highly effective tool for family protection, but its value relies on a clear, well-organized claims process. By systematically tracking your contract files, keeping your beneficiary designations updated, and understanding the underwriting timelines used by major carriers, you can eliminate administrative friction and ensure a seamless transfer of wealth.

Take the time to review your policy documentation today, map out your family’s actual liabilities using an interactive claims planner, and structure your protection to provide true financial peace of mind for your loved ones.