Securing a term life insurance policy is one of the most practical steps an income earner can take to safeguard their family’s financial future. For a locked period, usually 10, 20, or 30 years, you pay a stable monthly premium. In return, the insurance provider promises to pay a substantial tax free sum to your beneficiaries if you pass away while the policy is active.

But what happens if the years pass by, you remain healthy, and the policy reaches its expiration date? What happens when that final month closes?

Statistically, outliving a term life insurance policy is the most common outcome. According to historical actuarial summaries, more than 95% of individual term life policies expire without paying out a death benefit. This result means your risk management strategy worked exactly as planned: you protected your family during your peak financial liability years, and you survived the danger window.

However, letting a policy reach its expiration date without preparation can create an unexpected financial vulnerability gap. As healthcare spending trends climb, managing financial security in later years requires a clear understanding of your insurance alternatives. Let’s look at exactly what happens when your term policy expires, compare your financial options, and build a strategy to manage your long term liabilities.

The Immediate Financial Reality of Expiration

The moment your term insurance policy reaches its final calendar date, the initial insurance contract terminates. Here is the baseline reality of that transition:

The Death Benefit Ends: The insurance carrier is no longer under any contractual obligation to pay your beneficiaries if you pass away.

The Premium Outlays Stop: You are no longer required to make monthly premium payments.

No Accumulated Asset Value: Because term life insurance is designed as pure risk protection, it accumulates zero internal cash savings. When the term ends, you do not receive a refund of past premiums, unless you specifically purchased an expensive Return of Premium (ROP) rider at the start of your coverage.

For many households, reaching this milestone is a positive sign. It often aligns with entering retirement, paying off a home mortgage, and watching children reach financial independence. At this stage, you may no longer need life insurance because you have achieved a “self-insured” status.

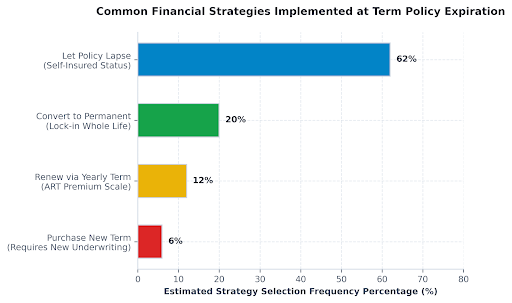

Common Strategies Implemented at Policy Expiration

To see how consumers manage this financial transition, review the strategy distribution chart below. It highlights the statistical frequency of choices made by policyholders as they reach the end of their term coverage.

Structural Comparison: Your Four Strategic Pathways

If your term policy is nearing its end and you still carry financial obligations, you have four distinct pathways to consider. Each path uses a different pricing index and underwriting framework.

Financial Option

Medical Exam Requirement

Premium Cost Adjustment

Primary Strategic Benefit

Long-Term Caveat

Pathway 1: Let the Policy Lapse

None; the coverage terminates automatically.

Drops to $0 per month immediately.

Saves premium capital for retirement portfolios.

Leaves dependents fully exposed to any remaining debts.

Pathway 2: Convert to Permanent

None; guaranteed approval without health checks.

Increases significantly (often 5x to 10x higher).

Locks in guaranteed lifelong coverage and cash value.

High premium outlays can strain fixed retirement cash flows.

Pathway 3: Annual Term Renewal

None; guaranteed under the original contract terms.

Escalates sharply every year based on current age.

Quickly becomes too expensive to sustain long term.

Pathway 4: Buy a New Term Policy

Mandatory paramedical exam and full health check.

Priced based on your current age and medical history.

Secures stable, locked rates for a new term window.

Developing a new health issue can cause a flat denial.

Pathway 1: Transitioning to a Self-Insured Status

The most cost-effective option when a term policy expires is simply allowing it to terminate as designed. This is the optimal approach if you have achieved self-insured status.

You have reached a self-insured status when your accumulated liquid wealth, retirement accounts, and home equity are large enough to support a surviving spouse or dependents without needing an insurance payout. If your home mortgage is fully paid off, your children are financially independent, and your funeral costs are covered by basic savings, paying for life insurance premiums is an unnecessary expense.

Pathway 2: Utilizing the Policy Conversion Rider

If you reach the end of your term and discover you still need coverage, your best option may be a built-in contractual feature called a Term Conversion Rider.

Most high quality term life insurance policies include a conversion rider that allows you to swap your temporary term policy for a permanent whole life or universal life policy without undergoing a new medical exam or answering any health questions. The insurance carrier is legally required to honor your conversion request and grant you the best possible risk tier rating you qualified for when you first bought the policy years prior.

The Financial Power of Guaranteed Conversion

This conversion feature is incredibly valuable if your health has declined since you first purchased the policy. Suppose you bought a 20 year term policy at age 35, qualifying for the top “Preferred Plus” pricing tier. At age 54, you develop a serious medical issue, such as type 2 diabetes or a cardiac irregularity, which would make you uninsurable on the open market.

By triggering your conversion rider before the term expires, you can lock in a permanent policy that lasts your entire life, backed by your original “Preferred Plus” risk status. While your premiums will increase substantially because permanent insurance is more expensive and you are now older, your coverage cannot be denied or table rated due to your health changes.

Pathway 3: The Pitfall of Yearly Renewable Term Extensions

If your term expires and you take no action, many modern policies feature an automatic safeguard called Annual Renewable Term (ART) or Yearly Renewable Term extension.

This feature keeps your coverage active so it does not drop instantly, requiring zero new medical checks. However, relying on this pathway for more than a few months is a severe financial mistake.

Under an ART extension, your premiums are recalculated every single year based directly on your current age. Because the insurance carrier must assume your health status has declined, they build massive risk margins into the new premium index.

Numerical Example of Annual Renewable Rate Escalation

Consider an individual whose fixed 20 year term policy covered $500,000 for a locked price of $45 per month. The moment the term ends and transitions to an automatic annual renewal track, the pricing scales predictably upward:

\text{Year 1 of ART Extension (Age 55)} = \$195 \text{ / month}

\text{Year 2 of ART Extension (Age 56)} = \$260 \text{ / month}

\text{Year 3 of ART Extension (Age 57)} = \$345 \text{ / month}

As illustrated by this compounding trend, the monthly cost quickly becomes unsustainable. ART extensions are designed strictly as a brief stopgap to keep you covered for a few months while you finalize a long term strategy. They are not a viable option for multi-year protection.

Pathway 4: Securing a Fresh Individual Policy

If you reach the end of your term policy and remain in excellent physical condition, you can apply for a brand new individual policy on the open market. This path allows you to secure much lower rates than a permanent policy conversion or an ART extension.

You can customize this new policy to fit your current life stage. Instead of buying another long 30 year policy, you can look at shorter coverage lengths tailored to your remaining obligations:

A 10 Year Term Policy: Ideal for matching the final decade of your working career, protecting your income until you reach full retirement age.

A 15 Year Term Policy: Perfectly suited to cover the remaining principal balance on a downsized home loan or a refinanced mortgage.

The only downside to this approach is that you must pass full medical underwriting checks again, including a new paramedical exam, blood panels, and an audit of your electronic medical records.

Implementation Strategy: Planning Your Next Steps

To protect your family from a coverage gap as your policy nears expiration, use this systematic approach to plan your transition:

Step 1: Review Your Current Financial Obligations

Document your household’s active liabilities. Check your remaining mortgage balance, assess your spouse’s retirement income security, and calculate your final funeral and estate administration costs.

Step 2: Confirm Your Policy’s Conversion Expiration Date

Do not assume you can wait until the final month of your policy to convert your coverage. Most insurers require you to trigger the conversion rider several years before the term ends, or before you reach a specific age limit (often age 65 or 70). Locate your original contract documents to confirm your exact conversion window.

Term Expiration Strategy Planner

Map your remaining financial liabilities and health markers to find your optimal pathway before coverage ends.

1. Your Current Horizon

Time left before your current fixed rate structure expires.

Mortgage principal, consumer debt, or required spousal income runway.

Have you developed new chronic medical conditions since buying the policy?

2. Recommended Strategic Path

Optimal Transition Pathway

Loading Pathway…

Urgency Priority Index

Analyzing window…

New Medical Underwriting Required:Checking…

Relative Premium Cost Profile:Checking…

Core Action Timeline window:Checking…

Evaluating macro financial risk profiles…

Step 3: Work with an Independent Broker

If you need to maintain coverage, consult with an independent insurance broker at least 12 months before your current policy expires. Independent brokers can evaluate your health profile anonymously across dozens of competing carriers, helping you find the most affordable way to protect your household.

Summary and Next Steps

Outliving your term life insurance policy means your long term risk management plan worked exactly as intended. However, managing the end of your policy requires proactive preparation. By systematically auditing your remaining liabilities, tracking your policy’s conversion windows, and evaluating independent coverage options early, you can build a stable financial plan that keeps your family fully protected.

Take the time to review your original policy terms today, map your real coverage needs using an interactive planner, and secure the right protection to maintain long term financial peace of mind.