Securing dependable financial protection is a vital objective for families across the nation. However, if you or a loved one manages a chronic health condition like type 2 diabetes, hypertension, or a history of cardiovascular recovery, the path to obtaining a policy can feel incredibly intimidating. Many individuals assume that an imperfect medical history automatically results in a flat coverage denial.

This assumption is a pervasive misconception that can leave households needlessly exposed to significant financial risk. The reality is that the commercial life insurance market has evolved rapidly over recent years. Driven by massive advancements in clinical tracking software, automated clinical underwriting tools, and expanded real-time electronic health data networks, insurance carriers have radically transformed how they measure risk.

While health insurance policies are strictly regulated under federal frameworks like the Affordable Care Act, life insurance companies operate on entirely different financial models. Life insurance providers use medical history evaluation to price contracts based on your statistical risk profiles. Securing coverage with a pre-existing medical history is highly achievable, provided you understand the specific underwriting guidelines used by major carriers. Let’s look at how insurers evaluate chronic health issues, compare your policy options, and map out a strategy to protect your family’s budget.

How Life Insurance Underwriting Measures Pre-Existing Conditions

To successfully navigate the application process, you must understand exactly how an insurance carrier assesses a pre-existing health condition. Underwriters do not simply see a diagnosis and make a decision. Instead, they look closely at the depth, control, and long-term stability of your health metrics.

Key Factors Evaluated by Insurance Underwriters

The Exact Timeline of the Diagnosis: Insurers evaluate exactly when you were first diagnosed. For many conditions, an extended history of stable metrics is viewed far more favorably than a highly volatile, recent medical diagnosis.

Clinical Treatment and Metric Control: Carriers look for consistent medical adherence. For example, an applicant with type 2 diabetes who maintains an HbA1c level below 6.5 through consistent medication and regular doctor checkups will secure substantially better rates than someone with erratic glucose readings.

Prescription Medication Histories: Automated clearinghouse systems allow underwriters to instantly audit your multi-year prescription history. They track drug classes, dosages, and compliance to evaluate the severity and stability of the underlying condition.

Secondary Lifestyle Risk Multipliers: Actuarial models analyze how your health history interacts with external lifestyle choices. Having a controlled chronic condition alongside a tobacco-user status or an elevated Body Mass Index (BMI) creates a compounded risk profile that can result in higher premium tiers.

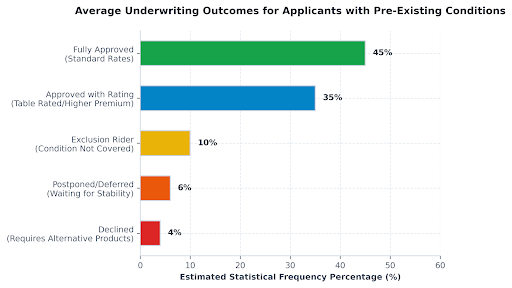

Underwriting Outcomes for Applicants with a Medical History

To see how applications with a pre-existing medical history typically settle across the broader insurance industry, review the outcomes distribution chart below. It highlights the statistical breakdown of how carriers categorize risk pools for individuals with an established health history.

Structural Comparison: Policy Pathways for Pre-Existing Conditions

When applying for coverage with a medical condition, you will typically choose between three primary policy pathways. Each structure uses a completely different underwriting framework and premium pricing index.

Operational Metric

Fully Underwritten Term Policy

Simplified Issue Life Policy

Guaranteed Issue Life Policy

Medical Exam Requirement

Mandatory paramedic visit (blood, urine, vitals).

No physical exam; relies on digital records.

No medical exam and zero health questions.

Data Underwriting Depth

High; searches full electronic records.

Moderate; checks prescription drug logs.

Zero checking; acceptance is fully automatic.

Average Premium Pricing

Lowest, provided condition control is verified.

Mid-tier; features built-in risk margins.

Highest premium per dollar of coverage.

Maximum Coverage Caps

High; scales into multi-million dollar limits.

Mid-tier; typically capped at $50,000 to $100,000.

Low-tier; strictly capped at $10,000 to $25,000.

Death Benefit Structure

Active immediately from day one of the policy.

Active immediately from day one of the policy.

Graded; requires a 2-year waiting window.

The Financial Impact of Table Ratings Explained

If you apply for a traditional term or whole life policy and your medical history carries an elevated risk profile, the carrier will frequently offer coverage through a Table Rating System.

Standard policies are distributed across tiers like “Preferred Plus,” “Preferred,” and “Standard.” When an applicant’s risk extends past the Standard profile, underwriters apply alphabetical or numerical table ratings (typically labeled Tables A through P, or Tables 1 through 16).

Each sequential table rating step adds a fixed percentage typically 25% to the standard baseline premium cost of the policy.

Numerical Example of Table Rating Escalation

Consider a 40-year-old applicant applying for a $500,000 20-year term insurance policy. If this individual had a completely perfect medical history, their base “Standard” premium might sit at $50 per month.

If their pre-existing condition results in a Table B (or Table 2) risk assessment due to slightly elevated health markers, the premium scales as follows:

Securing a policy with a Table B rating is slightly more expensive, but it remains a highly effective financial option. It allows you to lock in substantial, long-term coverage to protect your family’s peak liabilities, such as a home mortgage or future college tuition, without facing a flat application denial.

When Alternative Policies Become Essential

If a chronic condition is advanced or currently unstable, traditional fully underwritten policies may be postponed or declined. In these scenarios, alternative policy structures become crucial tools for family protection.

1. Simplified Issue Life Insurance

Simplified issue policies bypass the standard paramedic home visit. Instead, you complete a targeted health questionnaire, and the carrier uses real-time digital databases to check your prescription history and medical billing records. Because the insurer takes on slightly more unknown risk, premiums are higher than fully underwritten policies, but coverage can often be approved in minutes.

2. Guaranteed Issue Life Insurance

Guaranteed issue policies are designed as a reliable last resort for final expenses. They feature zero medical exams and ask absolutely no health questions. Acceptance is entirely automatic, provided you meet the basic age requirements (typically age 50 to 80).

To offset the high risk of automatic approval, these plans carry two built-in constraints: low coverage limits (usually capped at $25,000) and a graded death benefit structure. If you pass away from natural health causes during the first two years of the policy, your beneficiaries do not receive the full face amount. Instead, they receive a refund of all paid premiums plus interest, typically around 10%. Full coverage kicks in automatically once the initial two-year waiting window has passed.

Step-by-Step Security Strategy for Higher Approval Rates

To maximize your chances of policy approval at the lowest possible premium rates, use this systematic approach to plan your insurance application:

Step 1: Secure Your complete Medical Records

Request comprehensive documentation from your primary care physician. Gather your recent laboratory test readouts, complete prescription dosages, and notes verifying your treatment compliance. Having organized medical records shows underwriters that your health condition is being proactively managed.

Step 2: Utilize a Dedicated Independent Broker

Avoid applying directly to a single captive insurance carrier. Captive agents can only sell policies from their specific company, and different insurers use completely different guidelines to evaluate chronic illnesses. An independent broker can shop your anonymous health profile across dozens of major carriers, matching your medical history with the specific company whose actuarial tables are most favorable to your diagnosis.

Underwriting Risk Profiler

Estimate your likely life insurance approval pathway and premium pricing tier based on your current health history.

1. Your Health Profile

Time elapsed with stable lab results and unchanged medications.

2. Estimated Policy Pathway

Recommended Application Track

Loading…

Estimated Premium Risk Level

Evaluating…

Medical Exam Requirement:Checking…

Pricing Structure Index:Checking…

Broker Selection Strategy:Independent Match Required

Processing clinical indicators…

Step 3: Maintain Medical Compliance

Ensure you follow your prescribed medical treatments consistently. Underwriters look closely at regular doctor visits and stable laboratory trends. Maintaining good lifestyle choices and following your care plan directly translates to better risk ratings and lower long-term premium outlays.

Summary and Next Steps

Managing a pre-existing medical condition does not mean you have to leave your family unprotected. By tracking your health metrics, choosing the right policy structure, and working with independent brokers who understand specialized underwriting guidelines, you can secure an affordable policy that keeps your household safe.

Take the time to organize your medical records today, run your numbers through an interactive risk calculator, and secure independent protection that provides true financial peace of mind for your loved ones.