Navigating personal finance requires separating proven strategic blueprints from persistent cultural misconceptions. In few sectors are these misconceptions as financially destructive as in the life insurance market. Misunderstanding policy structures, underwriting parameters, or coverage timelines can easily cost your dependents hundreds of thousands of dollars in unbacked liabilities or wasted premium outlays.

The current financial climate makes accurate planning even more vital. Amid ongoing cost of living adjustments, elevated core consumer prices, and changing mortality trends, traditional family safety nets are facing unprecedented stress. Recent industry insights show that commercial carriers have adjusted their pricing index rules globally. This means that families operating on outdated advice face significant coverage gaps.

To secure your household’s long term financial stability, you must look past common marketing narratives and analyze the actuarial realities of modern insurance planning. Let’s break down the most pervasive life insurance myths, examine the actual data behind them, and establish an optimized framework to protect your family.

Myth 1: My Employer Group Policy Provides Enough Protection

The most widespread and dangerous misconception among corporate professionals is assuming that the complimentary group life insurance policy provided through their workplace benefits package offers a complete financial safety net.

While corporate packages frequently offer basic coverage equal to one or two times your annual salary, relying on this as your primary defense introduces severe long term risks:

The Portability Hazard: Group life insurance policies are almost always tied directly to your active employment status. If you experience a corporate downsize, change industries, or face a medical issue that forces you to leave the workforce, your coverage terminates immediately.

The Age and Health Trap: If you lose your workplace policy in your 40s or 50s and must transition to individual coverage, your new premiums will be substantially higher due to accumulated age and potential changes in your health.

Severe Capital Deficits: A payout equal to double your salary is quickly spent when managing a modern mortgage, clearing consumer student loans, and funding higher education tuition for a growing household.

Workplace group policies should be viewed as a supplemental benefit rather than the foundation of your family’s financial security.

Structural Comparison: Individual Policies vs. Employer Group Plans

To see how these two coverage models match up side-by-side, let’s examine their core characteristics, structural rules, and consumer protections.

Operational Vector

Independent Individual Policy (Term)

Employer Sponsored Group Plan

Ownership and Control

You own the contract directly; independent of your job.

The employer controls the master policy contract terms.

Asset Portability

Follows you across all career moves and retirements.

Terminates immediately upon leaving the company roster.

Premium Rate Structure

Locked in at purchase for the entire chosen term length.

Increases predictably as you enter higher age brackets.

Medical Underwriting

Full evaluation locks in low rates for healthy applicants.

No medical exam required; risk is averaged across the pool.

Coverage Capacity Caps

Scales up to multiple millions based on financial need.

Strictly capped, often at 1x to 2x your gross salary.

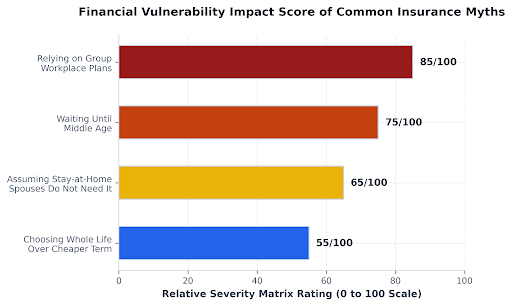

Visualizing the Impact of Financial Misconceptions

To visualize how different planning errors can impact your household’s safety net, review the vulnerability matrix model below. It illustrates the relative financial risk associated with the most common industry myths.

Myth 2: Life Insurance is Only for the Primary Breadwinner

Another common planning error is assuming that life insurance is only necessary for the family member who brings home the largest paycheck. This approach completely overlooks the immense economic value contributed by stay at home parents or secondary earners.

When a stay at home spouse passes away unexpectedly, the surviving parent must immediately outsource critical household responsibilities to commercial providers. The economic cost of replacing these daily contributions can be overwhelming:

Full Time Childcare Services: Securing professional childcare or nanny services for multiple children can cost tens of thousands of dollars annually.

Domestic Logistics and Management: Sourcing external help for household management, transportation, meal preparation, and property maintenance quickly creates a significant ongoing expense.

Career Impact on the Surviving Earner: The primary breadwinner may need to reduce their working hours, pass up promotions, or take an extended leave of absence to manage household transitions, directly reducing the family’s primary stream of income.

An accurate financial assessment must account for these hidden economic contributions, ensuring stay at home spouses carry adequate term coverage to shield the household from sudden lifestyle changes.

Myth 3: Whole Life Insurance is Always Superior to Term Insurance

The ongoing debate between Term Life and Permanent (Whole Life) insurance is often clouded by aggressive sales pitches. A common marketing narrative suggests that term insurance is a waste of money because it eventually expires, while whole life is framed as a superior asset because it builds cash value.

For the vast majority of standard income earners, this narrative is financially flawed. Let’s look at how the mechanics of these two models actually operate:

Term Life Insurance (Pure Risk Protection)

Term insurance operates like standard home or auto insurance. You pay a low monthly premium to secure coverage for a specific window of peak financial liability, such as a 20 or 30 year term while your mortgage is active and your children are growing up. If you do not pass away during the term, the policy expires. Because it includes no complex investment features, premiums are incredibly affordable.

Whole Life Insurance (Bundled Financial Products)

Whole life insurance provides lifelong coverage and bundles death protection with an internal cash value savings account. This added complexity makes whole life premiums 5 to 10 times more expensive than equivalent term coverage for the same death benefit. Furthermore, the internal fees, administrative costs, and surrender charges during the first decade of the policy often limit the growth rate of that cash value.

The Opportunity Cost of Whole Life

Consider a healthy 30 year old professional comparing their options for $500,000 of coverage:

Option A: Purchase a Whole Life policy for roughly $350 per month.

Option B: Purchase a 30 Year Term policy for approximately $35 per month, and direct the remaining $315 per month into low cost index funds inside a tax advantaged retirement account.

Over a 30 year horizon, the combined return from purchasing affordable term insurance and investing the premium savings independently typically far outpaces the cash value accumulation inside a whole life policy. Whole life insurance remains an effective tool for high net worth estate planning, but pure term insurance is usually the most efficient path for standard family protection.

Myth 4: You Should Always Buy Coverage Equal to 10 Times Your Salary

For decades, financial advice columns relied on a simple rule of thumb: Multiply your current annual salary by 10 to find your target coverage amount.

While this calculation is easy to perform, it is far too imprecise for modern financial planning because it ignores the actual liabilities unique to your household. A single earner with an $800,000 mortgage and three young children requires a completely different financial safety net than someone with an identical salary who rents an apartment and has no dependents.

To find your true insurance requirement, you should use the structured DIME Framework, which evaluates four key financial pillars:

Debt: Sum your outstanding consumer liabilities, including auto loans, student balances, and credit cards, to ensure they can be cleared immediately.

Income Replacement: Calculate your net annual take-home earnings and multiply it by the number of years required to support your youngest dependent until adulthood.

Mortgage Payoff: Factor in the full remaining principal on your home loans so your family can secure their housing stability clear of debt.

Education Funding: Allocate a target tuition buffer, typically $100,000 to $250,000 per child, to cover future college expenses.

Subtract your current liquid savings and active individual policies from this combined total to find your true target coverage amount. This systematically prevents both underinsurance and overpaying for unnecessary coverage.

Step-by-Step Security Strategy

To protect your family from the financial consequences of these common myths, follow this step-by-step approach to optimize your portfolio:

Step 1: Conduct a Comprehensive Liability Audit

Gather your financial statements and list your exact remaining mortgage principal, consumer debts, and baseline monthly household expenses. Note your children’s ages to map out your income replacement timeline.

Step 2: Calculate Your Core Coverage Needs

Move past generic salary multipliers and use an online DIME calculator to map your family’s actual financial obligations. Always round your final coverage target upward to build in a buffer for future cost of living shifts.

Family Protection Vulnerability Audit

Check your current exposure against common insurance myths to reveal hidden financial coverage gaps.

1. Financial Protection Survey

Workplace coverage usually ends immediately upon job or career change.

Replacing a non-working parent’s contributions costs tens of thousands annually.

Enter the total face amount of policies you own directly on the open market.

Sum your mortgage balance, non-mortgage debts, and long-term income replacement needs.

2. Risk Assessment Results

Vulnerability Score

0

Calculated Coverage Gap

$0

Secure (0)Moderate RiskHigh Vulnerability (100)

Audit Item Breakdowns

Workplace Portability Protection Status:Checking…

Spousal Economic Value Protection:Checking…

Total Unbacked Household Liabilities:$0

Evaluating survey fields…

Step 3: Lock In Independent Protection Early

Apply for an individual term insurance policy directly on the open market. Securing coverage while you are young and healthy allows you to lock in the lowest premium rates, ensuring your family’s safety net remains fully intact regardless of future job changes.

Summary and Next Steps

Protecting your family’s financial future requires replacing industry myths with clear, data-driven planning. By systematically calculating your actual household liabilities, acknowledging the economic value of both spouses, and choosing efficient policy structures, you can build a stable safety net that protects your dependents over the long term.

Take the time to evaluate your active coverage limits today, run the numbers for your family’s actual liabilities, and secure individual protection that provides true financial peace of mind.

")