When is the best time to purchase life insurance? Many young adults view life insurance as a financial milestone reserved for later in life, delaying the decision until middle age. This delay can be a very expensive financial mistake.

The life insurance industry is experiencing a significant shift in pricing dynamics. Driven by macroeconomic volatility, persistent cost of living adjustments, and updated mortality tables, standard insurance costs have steadily risen. Recent report findings indicate that major carriers have systematically revised underwriting criteria. These changes mean that waiting even a single year to secure individual health and financial protections can locks in permanently higher premium tiers.

The underlying math of financial underwriting remains simple: your premiums will never be lower than they are today. Let’s look at the best age to secure coverage, the financial math behind the cost of delay, and how to optimize your timeline to protect your household budget.

The Core Metric: Actuarial Risk and Your Age

To understand why waiting to purchase coverage is expensive, you must look at how underwriting models function. Insurance underwriting is built around actuarial probability tables that measure your statistical risk of mortality for any given year.

Every time you pass a birthday, your actuarial risk profile increments upward. For traditional term or permanent policies, carriers calculate a fixed premium based on your age and health status at the moment your application files are finalized. This rate remains completely locked for the entire duration of your policy term.

If you purchase a 20 year term policy at age 25, you lock in the low risk status of a 25 year old for the next two decades. If you delay that exact same purchase until age 35 or 45, you are forced to pay for the elevated risk baseline accumulated over that decade of delay.

This financial compounding effect means that the cost of life insurance scales predictably with age, with price hikes accelerating sharply as you pass major decade markers.

The Cost of Waiting Calculator

See exactly how delaying your life insurance purchase impacts your monthly premiums and long-term household budget.

1. Configure Comparison

2. Premium Impact Projection

Buying Today

$0/mo

→

Buying Post-Delay

$0/mo

Visual Premium Comparison

Rate Today$0

Delayed Rate$0

Increased Monthly Cost Multiplier:+$0 / mo

Total Wasted Premium Loss:$0

Calculating actuarial baseline parameters…

Structural Comparison: Cost Patterns Across Lifespan Decades

The financial consequences of delaying policy acquisition differ across the decades of your working life. Let’s examine how pricing and risk profiles change across different stages of adulthood.

Age Bracket

Typical Monthly Premium Factor

Primary Underwriting Risk Hurdle

Ideal Policy Type Considerations

The 20s (Age 20 to 29)

Lowest Baseline Rates

Early lifestyle habits and minimal medical history records.

30 Year Fixed Term policies to lock in entry level pricing long term.

The 30s (Age 30 to 39)

Moderate 30% to 50% Step Up

Early onset biometric changes like elevated blood pressure or cholesterol.

20 or 30 Year Term policies aligned with newborn child dependencies.

The 40s (Age 40 to 49)

Sharp 80% to 120% Escalation

Emergence of chronic metabolic markers and structural back issues.

15 or 20 Year Term policies focused on covering remaining home mortgages.

The 50s (Age 50 to 59)

Compounded 200%+ Rate Surge

Cardiovascular anomalies, early pre-diabetic diagnoses, and histories.

10 or 15 Year Term or specialized structural Permanent coverage layouts.

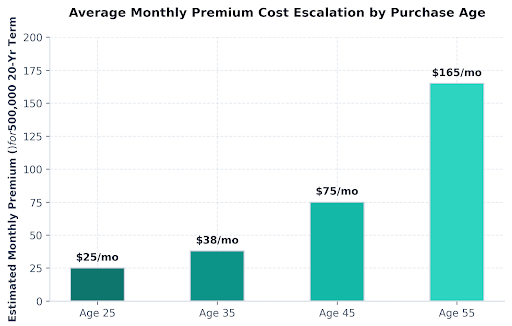

Visualizing the Price of Delay

To visualize how waiting can impact your monthly cash flow, review the premium distribution trend model below. It illustrates the typical trajectory of monthly premium escalation for a standard $500,000 policy based on your age at purchase.

The Compounded Math of Postponement

The cost of delaying life insurance is not a simple linear progression. Instead, it operates on a compounding scale. For every year you wait, your base rate increases by roughly 8% to 12% in your 30s, and jumps by 15% to 18% per year once you pass age 40.

Let’s examine a practical example using representative industry data for a standard healthy individual purchasing a $500,000 20 year term insurance policy:

Scenario A: Secure Policy at Age 25

A healthy 25 year old professional can easily secure a $500,000 20 year term plan for approximately $25 per month. Over the entire 20 year lifespan of the policy, the total premium investment equals:

If that same individual delays the decision until age 35, assuming their health status remains completely perfect, the monthly baseline premium increases to roughly $38. Over the 20 year lifespan of this delayed policy, the total premium investment becomes:

If the individual waits until age 45, the base rate climbs to approximately $75 per month. The total financial commitment over the 20 year span increases to:

By delaying the purchase from age 25 to age 45, the total cost for the exact same coverage triple. This premium difference represents money that could have otherwise been directed toward your retirement savings, investment portfolios, or principal mortgage payments.

The Unseen Danger: The Health Eligibility Trap

While the predictable annual price hikes are significant, the greatest financial danger of delaying life insurance is the Health Eligibility Trap.

Actuarial models assume you will develop more health issues as you age. If you wait to apply for life insurance, you run the risk of developing a medical condition before your policy is locked in. Common health developments can fundamentally alter your underwriting risk class:

Biometric Drift: Small, gradual increases in your resting blood pressure, fasting blood glucose, or lipid panels can drop your risk rating from “Preferred Plus” down to “Standard”. This drop can instantly add 40% to 60% to your base monthly premium.

Chronic Diagnoses: Developing a condition like type 2 diabetes, sleep apnea, or an autoimmune disorder will dramatically increase your premium rates across all major carriers.

Severe Health Events: Experiencing a significant health crisis, such as a cancer diagnosis or a cardiac event, can make you completely uninsurable on the individual open market.

Securing an individual policy while you are young and in peak physical condition creates a financial safety net that remains fully secure, even if your health changes down the road.

Why Employer Group Term Insurance is a Weak Foundation

A common reason people delay purchasing an individual life insurance policy is their reliance on corporate group term life insurance provided by their employer.

While corporate benefits packages often include a basic policy equal to one or two times your annual salary, relying on this coverage as your primary safety net introduces significant long-term risks:

Lack of Asset Portability: Group insurance policies are tied directly to your active employment. If you change jobs, face an unexpected corporate layoff, or experience a health issue that forces you to leave the workforce, your coverage terminates immediately.

The Age-Health Trap: If you lose your workplace coverage in your 40s or 50s due to a job change or health issue, purchasing an individual policy on the open market will be substantially more expensive than if you had secured a private, locked-in policy when you were younger.

Inadequate Coverage Caps: A basic policy covering two times your salary rarely provides enough capital to manage a modern mortgage, pay off long-term debts, and fund future education costs for a growing family.

Workplace policies should be viewed as a helpful supplement rather than the foundation of your family’s financial security.

Step-by-Step Optimization Strategy

To secure the highest coverage amounts at the lowest possible rates, use this step-by-step approach to plan your life insurance purchase:

Step 1: Establish Your Liabilities Baseline

Calculate your family’s true financial obligations, including remaining mortgage balances, outstanding student or auto loans, and the long-term income replacement runway required to support your dependents.

Step 2: Evaluate Your Coverage Options

Match your current life stage with the appropriate policy length. If you are in your 20s or 30s with a fresh mortgage or young children, a 30 year term policy offers an efficient way to lock in low premium rates through your peak financial liability years.

Step 3: Secure Independent Coverage

Apply for your policy independently rather than through employer pools. This ensures your coverage remains fully active regardless of job changes or career transitions, providing stable, long-term protection for your family.

Summary and Next Steps

When it comes to purchasing life insurance, waiting rarely pays off. Securing coverage when you are young and healthy allows you to lock in the lowest possible premium rates, protecting your long-term household budget.

By calculating your financial obligations early and locking in an individual term policy, you can build a stable financial foundation that protects your dependents, providing lasting peace of mind for decades to come.

")