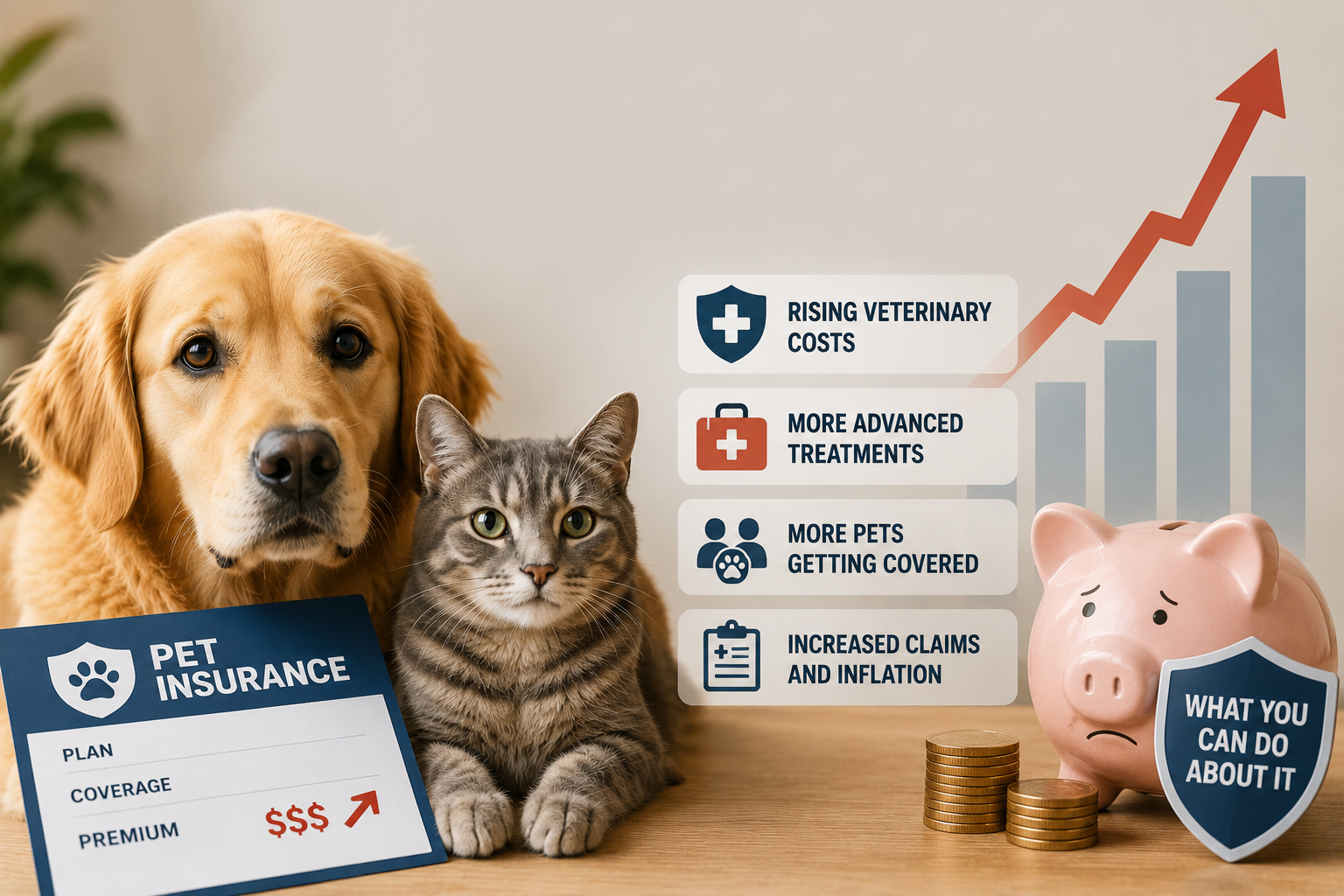

The global landscape of domestic veterinary medicine has undergone a monumental paradigm shift over the past decade. Today, companion animals are firmly cemented as primary family members, leading to unprecedented demands for human-grade healthcare. While modern advancements mean that conditions once considered terminal are now highly treatable, this therapeutic revolution comes with a stark reality: soaring veterinary operational costs.

As a consequence, pet parents worldwide are opening their renewal notices to find substantial rate hikes. If you have recently discovered that your monthly dog or cat insurance premium has jumped by 15%, 20%, or even 35%, you are not alone.

Understanding the precise economic, technological, and actuarial drivers behind these rising costs is the first step toward reclaiming control of your household budget. This comprehensive analysis breaks down exactly why pet insurance premiums are increasing globally and provides practical strategies to help you maintain vital coverage without sacrificing your financial stability.

Cost Management Simulator

Premium Inflation Optimization Tool

Simulate structural premium inflation drivers and instantly test policy adjustments to counter rate increases.

1. Current Cost & Inflation Factors

2. Proactive Optimization Levers

3. Cost Assessment Output

Estimated Simulated Premium

\$52.00 /mo

Optimized Setup Active

Age Risk Adjustment:Baseline

Breed Risk Loading:None (Mixed Base)

Deductible Offset Benefit:-\$10.00

Optimization Recommendation: Your chosen settings keep premiums predictable. Maintaining an adult baseline policy protects against upcoming lifelong chronic conditions.

1. The Core Economic Drivers of Premium Inflation

Insurance rates do not rise arbitrarily. They are directly tied to property-casualty insurance principles, where premiums must accurately reflect the total volume and monetary value of paid claims.

The Veterinary Care Consumer Price Index (CPI)

While general consumer inflation impacts everyday household items, medical inflation within the veterinary sector has risen at a much faster pace. The costs of advanced diagnostics, pharmaceutical supplies, and specialized veterinary equipment have reached historic highs.

The Veterinary Workforce Crisis

A major structural factor driving up clinic operational costs is a severe, systemic shortage of qualified veterinary professionals. This workforce squeeze includes both licensed DVMs (Doctors of Veterinary Medicine) and registered veterinary technicians. To attract and retain essential medical staff in a highly competitive market, animal hospitals have had to implement substantial salary increases and enhanced benefit programs. These higher labor costs are naturally reflected in the final invoices presented at the clinic front desk.

2. The Technological Revolution in Veterinary Medicine

The sophistication of modern veterinary medicine is a primary driver behind rising insurance premiums. The line between human hospitals and advanced veterinary referral centers has completely blurred.

Specialized Diagnostics and Therapeutics

Treatments that were unimaginable for companion animals twenty years ago are now standard procedures. These advanced medical interventions include:

Oncology and Immunotherapies: Linear accelerators for targeted radiation therapy and custom monoclonal antibody treatments for canine atopic dermatitis or feline arthritis.

Advanced Diagnostic Imaging: High-field MRI sequences and 64-slice CT scans used to identify complex neurological issues or subtle soft-tissue changes early.

Complex Orthopedics: Advanced procedures like Tibial Plateau Leveling Osteotomy (TPLO) for cranial cruciate ligament tears, or comprehensive total hip replacements using titanium implants.

The Financial Ripple Effect

When a diagnostic tool or surgical procedure becomes widely available, its usage rate among pet owners increases. Because pet insurance plans typically cover a set percentage of these invoices (often 70% to 90%), the average amount paid out per claim rises significantly. Underwriters must adjust base premium rates across entire regional groups to keep pace with these expanding clinical capabilities.

3. How Actuarial Risk Profiles Evolutionize With Age

A common point of confusion for pet parents is why their premiums increase year after year, even if their specific dog or cat has never filed a single medical claim. This occurs because pet insurance pools collective risk across broad categories.

As an animal ages, its statistical probability of requiring medical care follows an exponential curve. Actuarial charts demonstrate that while a young animal primarily faces unpredictable accident risks, aging animals regularly develop complex, long-term chronic conditions.

Because chronic conditions require ongoing, lifelong medical support rather than a single treatment, an older pet represents a higher long-term financial commitment for an insurer. Your premium increases as your pet transitions into these higher-risk age groups.

4. Current Market Shifts and Industry News

The pet health insurance sector is experiencing rapid changes as it adapts to new economic pressures. According to recent research data published by the Dog Aging Project Consortium, there is a direct correlation between advanced companion animal age and the rising complexity of multi-organ veterinary interventions. Their data highlights that as modern veterinary care extends the canine lifespan, the long-term management of overlapping chronic conditions creates an extended window of medical need.

At the same time, the corporate structure of veterinary medicine is undergoing an unprecedented shift. Independent, family-owned veterinary clinics are increasingly being purchased by large private equity groups and consolidated veterinary networks.

This trend toward corporate consolidation often leads to standardized, centralized pricing structures across regional networks. This corporate shift reduces a consumer’s ability to shop around for lower-cost local care, which ultimately places upward pressure on insurance premium baselines.

In response to these market challenges, forward-thinking insurance providers are introducing updates to traditional policy frameworks. As detailed by Petsy Insurance Insights, companies are rolling out customizable policy features designed to give consumers greater control over their monthly premiums. These modern policies allow pet parents to dynamically adjust their coverage parameters, providing a balanced way to manage rising costs without dropping coverage entirely.

5. Breed-Specific Risks and Regional Rating Variables

Your premium rate is calculated using a complex matrix of risk factors that goes far beyond your pet’s age. Two of the most significant variables are your pet’s genetic breed profile and your specific geographic location.

Genetic Predispositions and Actuarial Mapping

Purebred animals carry specific genetic profiles that make them more susceptible to certain conditions. Insurance companies analyze these breed-specific risks when setting premium levels.

For instance, deep-chested giant breed dogs—such as Great Danes, Irish Wolfhounds, and Standard Poodles—possess an elevated risk for Gastric Dilatation-Volvulus (GDV), commonly known as bloat. This life-threatening condition requires immediate, high-cost emergency surgery.

Similarly, brachycephalic (flat-faced) dog breeds like French Bulldogs, English Bulldogs, and Pugs face significant risks for Brachycephalic Obstructive Airway Syndrome (BOAS).

Because treating these conditions involves significant clinical expense, purebred animals carry a higher baseline premium compared to mixed-breed pets, whose wider genetic diversity makes them less prone to these predictable hereditary issues.

Postal Code Variations

Geographic location plays a surprisingly large role in your monthly premium costs. Veterinary clinics in major metropolitan areas face higher commercial rents, steeper property taxes, and elevated competitive wages for staff. If you live in an urban center with a high cost of living, your local veterinary invoices will reflect those overhead expenses. Insurance companies map these costs by postal code, adjusting premiums upward for residents in high-cost veterinary regions.

6. Proactive Strategies: What You Can Do to Lower Your Premium

When faced with a significant premium increase, your first instinct might be to cancel the policy entirely. However, completely dropping coverage leaves you fully exposed to unpredictable emergency veterinary bills. Instead, you can use several proactive strategies to adjust your existing policy and lower your monthly premium to a manageable level.

1. Optimize Your Annual Deductible

The most effective way to lower your monthly insurance premium is to adjust your annual deductible upward. If your policy is currently set to a $250 deductible, raising it to $500 or $1,000 can result in an immediate reduction in your monthly payment.

Choosing a higher deductible means you will cover more of the initial costs during a medical crisis out of pocket, but it successfully lowers your fixed, ongoing monthly expenses while keeping major catastrophe coverage firmly in place.

2. Modify Your Co-Insurance Reimbursement Level

Most top-tier pet insurance providers offer flexible reimbursement choices, typically 90%, 80%, or 70%. If you are currently on a 90% reimbursement plan, dropping down to an 80% or 70% level will noticeably lower your premium rate. While you will be responsible for a slightly larger share of the final clinic bill, your policy will still shield your household budget from the devastating impact of a major multi-thousand dollar emergency veterinary bill.

3. Remove Optional Routine Wellness Add-ons

Many base pet insurance policies include optional add-on riders that cover routine wellness care, such as annual vaccinations, dental cleanings, and flea or tick preventatives. While these add-ons are convenient, they are rarely cost-effective over the long term.

Insurers typically price these wellness riders to match the exact financial value of the care provided, meaning you are essentially paying for routine care in installments through your premium. Removing these wellness add-ons and paying for routine care out of pocket allows you to keep your base insurance policy focused purely on unexpected, high-cost accidents and illnesses.

4. Ask About Available Discounts

Many pet insurance companies offer structural discounts that are not automatically applied to your account. When reviewing your policy, look into these common discount opportunities:

Multi-Pet Discounts: Many providers offer a 5% to 10% premium reduction if you enroll multiple dogs or cats under the same household account.

Annual Payment Incentives: Paying your entire annual premium upfront in a single installment rather than through monthly billing often eliminates installment fees and lowers your overall cost.

Professional Affiliation Discounts: Several insurers offer premium discounts for active-duty military members, veterans, healthcare workers, rescue shelter volunteers, or members of specific professional alumni networks.

7. Step-by-Step Guide to Reviewing Your Policy

Step 1: Audit Your Claims History

Review your pet’s medical history and past claims. If your pet has developed a chronic illness like diabetes or arthritis under your current policy, that condition is now a pre-existing condition. This means you should stay with your current provider, as switching companies would cause that chronic illness to be permanently excluded from your new coverage.

Step 2: Evaluate Your Emergency Savings

Take a look at your household liquid savings. Determine if you can comfortably cover a $500 or $1,000 deductible on short notice during an unexpected medical crisis. If you have the savings buffer to handle a higher deductible, you can confidently adjust your policy settings to reduce your monthly premium payments.

Step 3: Use Online Customer Portals to Customize Options

Log into your insurance provider’s online customer dashboard or call their customer service line. Experiment with different combinations of annual deductibles and reimbursement percentages to find the ideal balance that keeps your monthly premium within your budget while maintaining robust safety coverage.

Step 4: Avoid Complete Coverage Lapses

Make sure to keep your base policy continuously active. Letting your policy lapse, even for a short time, resets your coverage baseline. Any minor illness or injury documented in your pet’s veterinary files during the lapse will be treated as a pre-existing condition when you reinstate coverage, leaving you exposed to future out-of-pocket costs.

Critical Takeaway: Rising pet insurance premiums are a direct reflection of the growing costs and advanced capabilities of modern veterinary care. Rather than canceling your policy and taking on full financial risk alone, you can successfully counter rising costs by strategically adjusting your deductibles, modifying your reimbursement levels, and focusing your policy entirely on unexpected accidents and illnesses.