Selecting the right life insurance plan is one of the most critical elements of a robust personal financial strategy. Yet, millions of households navigate this process using outdated rules of thumb or arbitrary guesswork. Buying too little coverage leaves your dependents exposed to sudden, devastating lifestyle changes, while purchasing an oversized policy drains your monthly investable cash flow through unnecessarily high premiums.

The macroeconomic environment has significantly complicated this decision. With persistent cost-of-living adjustments, rising higher education tuition rates, and average fixed mortgage balances remaining near record highs, traditional calculations no longer provide an adequate safety net. According to recent demographic surveys, a substantial segment of income earners remain underinsured, mistakenly relying solely on basic group policies provided by their employers.

To accurately determine your ideal coverage amount, you must look past generic formulas and build a personalized calculation based on your current liquid assets, long-term debts, and specific family dynamics.

The Flaw of Traditional Rules of Thumb

For decades, commercial insurance agents popularized the standard rule of thumb: Multiply your current gross salary by 10.

While this calculation is incredibly simple to perform, it is fundamentally flawed because it ignores the unique financial complexities of individual households. A rigid salary multiple completely overlooks critical variables that change from family to family:

Current Debt Structures: A family carrying an $800,000 fixed-rate mortgage requires a vastly different financial cushion than a family renting an apartment or owning their home clear of debt, even if both primary earners draw identical salaries.

Dependent Ages and Timelines: The financial runway required to support a newborn child until they reach financial independence is vastly longer than the timeline needed to support a teenager who is already entering college.

Spousal Income Dynamics: If a surviving spouse earns a high salary, the household’s income-replacement target is completely different from a family that relies entirely on a single breadwinner.

Relying on a simple 10x multiple can result in structural underinsurance for young families with high debt loads, or expensive overinsurance for older households nearing retirement.

Structural Comparison: The Two Leading Assessment Methods

When moving away from generic multipliers, financial planners generally utilize one of two core analytical methodologies to calculate a household’s true life insurance target.

Operational Metric

The DIME Method (Structured Blueprint)

The Capital Needs Analysis (Dynamic Cash Flow)

Primary Structural Focus

Categorical allocation based on four fixed liabilities.

Long-term net present value projection of family cash flow.

Complexity Level

Moderate; straightforward to calculate on a spreadsheet.

Advanced; requires discounting future values for inflation.

Ideal User Profile

Households with standard debts, young children, and clear expenses.

High-net-worth individuals, complex estates, and business owners.

Treatment of Assets

Subtracts current liquid balances at the end of the math loop.

Continuously offsets obligations against investment growth rates.

Flexibility Margin

Rigid; assumes fixed targets for debts and final expenses.

High; adapts dynamically to changing lifestyle expectations.

Method 1: The DIME Framework Explained

1. Debt (Non-Mortgage Liabilities)

Sum every dollar of immediate consumer liability your family owes. This category must include auto loans, credit card balances, personal lines of credit, and outstanding student loans. The goal is to provide enough immediate cash to eliminate these high-interest obligations upon your death, immediately lowering your family’s monthly cost of living.

2. Income Replacement

Determine how many years your family will need to replace your salary to maintain their current quality of life. A standard guideline is to multiply your current net income by the number of years until your youngest child graduates from university or reaches adulthood.

3. Mortgage Liquidation

Your home’s remaining mortgage principal is typically the largest single expense your family will face. Including the entire remaining mortgage balance in your life insurance policy allows your family to pay off the home immediately, securing their housing stability and removing monthly rent or mortgage payments from their future expenses.

4. Education Funding

Calculate the projected cost of higher education for your children. With public and private university costs rising consistently, factoring in tuition, room, and board is essential. A common target is to allocate $100,000 to $250,000 per child, depending on whether you plan to cover public in-state or private out-of-state tuition.

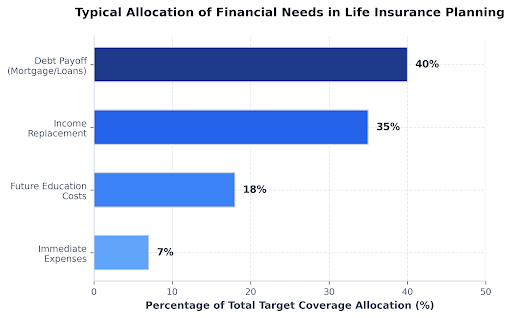

Visualizing Asset Allocation Needs

To see how these categories typically distribute within a balanced financial safety net, review the typical breakdown model below. It illustrates how total insurance capital is generally allocated to protect a standard household.

Method 2: Capital Needs Analysis (The Advanced Framework)

While the DIME framework provides an excellent structural baseline, advanced financial planning frequently utilizes Capital Needs Analysis. This method views your family as a functioning business entity, projecting long-term income, inflation, and investment yields to find the exact net present value of your future financial obligations.

Instead of simply accumulating fixed debt totals, this approach models how capital will be spent over time. It assumes the insurance payout will be placed into a diversified investment portfolio, generating regular returns to support the family while the principal is gradually drawn down.

The Capital Needs Equation

To calculate your coverage target using this model, you can express the mathematical relationship through this formula:

\text{Target Coverage} = \left( \frac{\text{Annual Income Needed} - \text{Surviving Income}}{\text{Real Rate of Return}} \right) + \text{Immediate Liabilities} - \text{Liquid Assets}

Where the Real Rate of Return represents your portfolio’s expected investment yield adjusted for inflation. This method ensures your family’s purchasing power is fully protected against rising consumer prices over a multi-decade timeline.

The Hidden Trap: Over-Relying on Employer Group Policies

One of the most common mistakes working professionals make is assuming they are fully protected by the complimentary group life insurance policy provided through their employer.

While corporate benefits packages often include a basic policy equal to one or two times your annual salary, relying on this coverage as your primary safety net introduces significant risks:

Lack of True Portability: Group life insurance policies are almost always tied directly to your employment status. If you change jobs, face a corporate layoff, or experience an extended medical issue that forces you to leave the workforce, your life insurance coverage terminates immediately.

The Age-Health Trap: If you lose your workplace coverage in your 40s or 50s, purchasing an individual policy on the open market will be substantially more expensive than if you had secured a private, locked-in term policy when you were younger and healthier.

Inadequate Benefit Ceilings: A policy that covers two times your salary rarely provides enough capital to manage a mortgage, pay off consumer debts, and fund future education costs for a growing family.

Workplace policies should be viewed as a supplemental benefit rather than the foundation of your family’s financial security.

Choosing Your Policy Structure: Term vs. Permanent

Once you have calculated your ideal coverage target, you must decide how to structure your policy. The industry is divided into two primary product categories:

1. Term Life Insurance (Pure Protection)

Term life insurance covers you for a specific window of time, typically 10, 15, 20, or 30 years. You choose a term length that matches your family’s peak financial liabilities such as the length of your mortgage or the years until your children graduate from college.

Because term insurance has no investment component and only pays out if you pass away during the active term, it is incredibly cost-effective. This allows young families to secure substantial coverage amounts without straining their monthly budget.

2. Permanent Life Insurance (Whole or Universal Life)

Permanent policies provide lifelong coverage and include a cash value component that grows over time. While this cash value can be accessed via policy loans or withdrawals during your lifetime, permanent insurance carries premiums that can be 5 to 10 times more expensive than equivalent term policies.

For the vast majority of standard income earners, purchasing an affordable term policy and investing the premium savings into tax-advantaged retirement accounts yields superior long-term wealth accumulation.

Step-by-Step Implementation Strategy

To move from analysis to execution, follow this definitive implementation checklist:

Step 1: Gather Your Current Financial Statements

Log into your financial portals and document your exact remaining mortgage principal, outstanding consumer debts, and liquid savings accounts. Note your household’s baseline monthly expenses to understand your true income-replacement needs.

Step 2: Run Your Numbers Through an Interactive Model

Use the calculation parameters from the DIME framework or Capital Needs Analysis to determine your target coverage amount. Always round your final coverage figure upward to provide an extra buffer for unexpected future inflation or medical expenses.

DIME Life Insurance Needs Calculator

Systematically estimate your household’s true coverage target by mapping your long-term liabilities.

1. Input Financial Parameters

Credit cards, auto loans, student balances

Your annual net take-home earnings target

Years until dependents reach self-sufficiency

Total remaining balance on home loans

Allocated tuition/living capital for all children

Cash, current investments, active workplace coverage

2. Target Coverage Required

Net Target Life Insurance Need

$0

Component Allocation Bar

(D) Debt Liquidation

$0

(I) Income Replacement

$0

(M) Mortgage Payoff

$0

(E) Education Funding

$0

Less: Existing Assets Asset Offset

-$0

Analyzing configurations…

Step 3: Align Your Coverage with Major Life Events

Your life insurance needs are not static. Significant life changes such as buying a new home, having another child, receiving a substantial salary increase, or paying off long-term debts should prompt a review of your coverage. Re-evaluating your insurance portfolio every three to five years ensures your protection remains aligned with your family’s actual liabilities.

Summary and Next Steps

Determining your life insurance requirement requires moving past generic assumptions and evaluating your family’s actual financial liabilities. By systematically tracking your debts, income replacement timelines, mortgage balances, and education targets, you can build a customized plan that protects your dependents without overcharging your monthly cash flow.

Securing an independent individual policy ensures your family’s financial safety net remains fully intact, completely independent of your employment status, providing lasting peace of mind.