When you establish a life insurance portfolio, you are engineering a precise mathematical solution to a future human crisis. You calculate the exact capital required to discharge your home mortgage, replace your annual salary for ten consecutive years, and fund tuition records for your children. You sign the contract, set up your monthly premium invoices, and take comfort in knowing that your family’s financial security is secured.

However, financial planning does not happen in an economic vacuum. Over a long horizon, a quiet macroeconomic force steadily chips away at the real-world utility of your policy. That force is inflation.

As we navigate 2026, the global financial landscape is coming out of a highly volatile macroeconomic cycle. Central banks around the world, including the United States Federal Reserve, have spent several years fighting persistent price increases. While headline inflation measures like the Consumer Price Index (CPI) have pulled back from their historic highs, the compounding effect of structural price increases remains permanently baked into the cost of goods, services, and general living overhead.

If you purchased a fixed $500,000 term life insurance policy a decade ago, that face value remains identical on paper. In the real world, however, its actual purchasing power has significantly degraded. This extensive guide uncovers the structural impact of inflation on life insurance assets, analyzes the differences between term and permanent coverage vehicles, and outlines actionable financial strategies to future-proof your family wealth insulation layer.

The Real-World Velocity of Purchasing Power Degradation

To understand how inflation shifts your protection landscape, you must distinguish between nominal value and real value. Nominal value is the absolute dollar number printed on your policy documentation. Real value is the volume of tangible commodities, housing, utilities, and education that those dollars can buy in the future.

When inflation stays steady at an annual rate of 3%, the nominal dollars do not change, but their purchasing power drops. The chart below tracks the real-world purchasing power erosion of a fixed $1,000,000 life insurance policy over a 30-year timeframe, assuming a constant 3% compound annual inflation rate.

This structural decay means that a policy designed to fully replace your income and clear your family debts could leave your beneficiaries facing a major funding gap if it is accessed 20 years down the road. The expenses you planned for, such as standard groceries, healthcare maintenance, and municipal property taxes, will all demand significantly more cash than your original framework assumed.

Life Insurance Inflation Erosion Simulator

Visualize how compounding macroeconomic inflation degrades the real-world purchasing power of your fixed death benefit over time.

1. Simulation Parameters

The nominal dollar payout printed on your current life insurance contract.

Historically, core inflation averages around 3%, but volatile economic cycles can spike this baseline higher.

Select your current policy adjustment framework to view tactical advice.

2. Purchasing Power Projections

Real Purchasing Power in 30 Years

$0

0% Real Value Loss

Erosion Timeline (Real Utility vs Time)

Year 10: $0

Year 20: $0

Year 30: $0

Strategic Wealth Advisory

Analyzing historical cost curves…

How Inflation Impacts Different Insurance Models

The structural impact of inflation depends heavily on whether your risk allocation uses a Term Life or a Permanent Cash-Value life insurance contract.

1. Term Life Insurance Frameworks

Term life insurance provides simple, high-limit death benefit protection for a predefined timeline, such as 10, 20, or 30 years. It features flat premium structures and a flat nominal death benefit payout.

The Exposure Path: Term insurance is highly vulnerable to inflation because it offers no internal growth mechanism to counter rising costs. If you buy a 30-year term policy to cover your family’s needs while your children grow up, the real value of that protection will drop every single year.

The Premium Benefit: On the other side of the ledger, inflation actually provides a minor benefit regarding your premium outlays. Because your monthly premium is locked at a fixed nominal rate for the life of the term, you pay your bills over time with dollars that are worth less than the dollars you used when you opened the policy.

2. Permanent and Cash-Value Insurance Models

Permanent life insurance policies, such as Whole Life, Universal Life (UL), or Indexed Universal Life (IUL), combine a traditional death benefit with an internal cash-value account that accumulates capital over time.

Traditional Whole Life: These frameworks often struggle in inflationary environments if their internal growth rates fail to outpace macro CPI tracking metrics. However, if your policy pays non-guaranteed dividends, you can optimize your setup by redirecting those payouts to purchase paid-up additions (PUAs). This automatically scales your total death benefit upward over time without requiring new medical exams.

Universal Life and Variable Options: Universal life frameworks offer more flexible premium structures. Variable Life models allow you to allocate your cash value across equity and bond sub-accounts. Because corporate equities often adjust their pricing power alongside rising costs, a properly managed variable policy can serve as an active hedge against inflation, keeping your cash value aligned with broader market shifts.

Technical Allocation Match: Rebalancing Your Capital Core

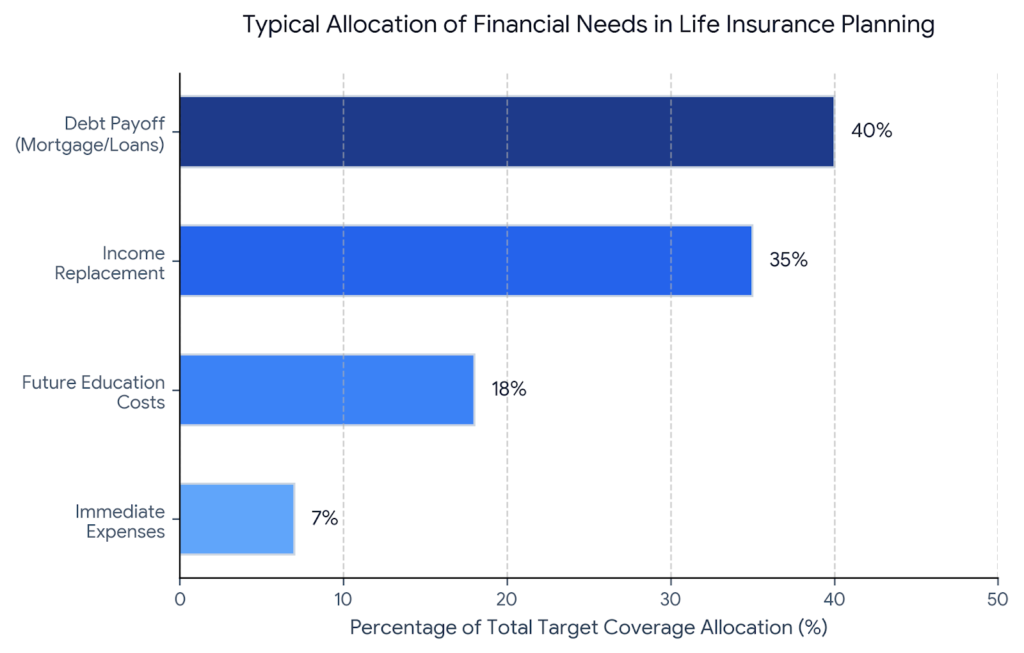

To offset the eroding effects of inflation, it helps to understand where your insurance proceeds are typically directed. This distribution chart maps out the key financial obligations that make up a standard long-term family protection plan.

By evaluating these specific categories, you can pinpoint exactly where inflation poses the greatest threat. For instance, while a fixed mortgage balance remains stable over time, your family’s ongoing income replacement needs and future college tuition goals will face significant upward price pressure.

The table below breaks down how these different financial liability categories respond to inflation over time.

Financial Liability Category

Inflation Sensitivity Index

Long-Term Strategic Risk Level

Recommended Protective Action

Fixed Commercial/Home Mortgages

Extremely Low

Low (Nominal balance remains fixed)

No adjustment required; regular amortization handles this.

Family Income Replacement Pool

High

Severe (Cost of living trends up)

Apply a 3% compounding factor to your annual income targets.

Higher Education / Tuition Funds

Very High

High (Tuition often outpaces base CPI)

Utilize dedicated investment engines or inflation riders.

Immediate Final/Funeral Expenses

Moderate

Medium (Service fees rise gradually)

Review capital cushions every five years to match local rates.

Navigating the 2026 Insurance Landscape: News and Carrier Adjustments

The shifts in global financial markets have caused life insurance carriers to adjust their risk modeling. According to recent life insurance industry reports from major research firms like Conning and the Swiss Re Institute, life insurance companies are actively re-pricing their long-term products to account for higher baseline operational overhead.

Rising Premium Benchmarks

Because insurers run on significant administrative capital, the increased costs of labor, software, data security, and corporate overhead have filtered into new policy pricing. While existing term policies remain locked by contract, individuals shopping for new coverage in 2026 are facing higher baseline premiums for identical coverage levels compared to a few years ago.

Increased Scrutiny on Cash-Value Projections

Carriers are also facing stricter regulations regarding how they present future cash-value growth. Regulatory adjustments from state insurance commissioners now require life insurance illustrations to show conservative return models. This change protects consumers from overly optimistic projections, ensuring that policyholders have a realistic view of how their cash value will accumulate in various economic environments.

Actionable Strategies to Future-Proof Your Coverage

You do not have to watch inflation erode your family’s protection. You can use several strategic planning methods to ensure your policy retains its intended utility over the long haul.

Strategy 1: Attach an Inflation Rider

Many insurance carriers offer a Cost of Living Adjustment (COLA) rider when you set up your initial policy. This rider automatically scales your total death benefit upward every year by a specified percentage, typically tracking the CPI or a fixed benchmark like 3% or 5%.

The best part of a COLA rider is that these coverage increases occur automatically, without requiring you to undergo new medical checkups or submit updated medical records. This ensures you maintain full financial protection even if your health profile changes later in life.

Strategy 2: Implement the “Laddering” Method

If you want to avoid paying for a costly permanent policy or expensive riders, you can use a strategic technique called term laddering. Instead of relying on a single large policy, you purchase multiple smaller term policies with staggered expiration dates.

Laddering allows you to front-load your highest level of financial protection during your early family-building years when inflation exposure is most volatile. As your children grow up, your mortgage gets paid down, and your personal investment portfolios grow, you can let older policies expire naturally, keeping your premium costs closely aligned with your actual liability shifts.

Strategy 3: Conduct a Mandatory Triennial Review

A life insurance portfolio should never be a set-it-and-forget-it asset. Every three years, schedule a formal review of your coverage alongside your household balance sheet.

Calculate your family’s current annual cost of living. If your household expenditures have scaled significantly due to lifestyle upgrades or inflation, work directly with an independent broker to secure a supplemental low-cost term policy to fill the gap, keeping your total safety net intact.

Summary and Key Takeaways

Inflation is an invisible but constant variable in long-term financial planning. While a fixed life insurance policy provides vital peace of mind today, ignoring the steady erosion of its purchasing power can leave your loved ones under-protected when they need it most.

By understanding how inflation shifts different insurance models, utilizing strategic options like COLA riders or term laddering, and running regular coverage checks, you can insulate your wealth layer from changing economic trends. Take control of your risk planning, adjust for long-term price paths, and ensure the financial legacy you leave behind retains its full power for the next generation.