Welcoming a new child brings tremendous joy alongside a fundamental shift in your personal financial obligations. As a young parent, your primary focus centers on daily care, pediatric visits, nursery configurations, and managing early childhood development milestones. Amid these immediate logistics, establishing a long term wealth protection framework frequently slips down the priority queue.

Postponing this protection can leave your household exposed to devastating financial vulnerability. The modern economic landscape presents unique structural hurdles for growing families. With persistent cost of living adjustments, elevated property prices, and rising higher education tuition rates, the financial margin for error has narrowed considerably. Recent actuarial surveys indicate that a majority of millennial and Gen Z parents operate with a significant life insurance protection gap, leaving their dependents vulnerable to unbacked liabilities.

The core reality of life insurance underwriting remains simple: your premiums will never be more affordable than they are when you are young, healthy, and entering parenthood. Let’s look at the operational mechanics of building a protection plan, compare product options, and establish an optimized framework to safeguard your family.

The Macroeconomic Stress Facing Young Families

To understand why traditional, static insurance assumptions no longer suffice, you must evaluate the changing financial baseline of modern households.

According to long term macroeconomic data, the core cost metrics that define family stability have outpaced median wage growth over the past decade. Buying a home requires taking on larger mortgage principals. Concurrently, raising a child from birth through age 17 requires substantial capital before factoring in university funding.

If a household’s primary income stream terminates unexpectedly, surviving spouses are immediately forced to manage these large, fixed obligations on a diminished cash flow. Relying solely on standard corporate benefits packages rarely offers a sufficient long term buffer. Securing an independent individual life insurance policy acts as a vital counterweight, absorbing financial shockwaves and ensuring your family’s lifestyle remains fully secure.

Structural Comparison: Individual Term vs. Corporate Group Protection

Many working professionals fall into the trap of assuming they are fully insulated because they receive complimentary life coverage through their employer’s open enrollment benefits package. Let’s examine how workplace plans compare to private policies.

Operational Vector

Independent Individual Term Policy

Employer-Sponsored Group Plan

Contract Portability

Follows you across all job changes, corporate layoffs, and career moves.

Terminates immediately upon leaving the active company payroll roster.

Premium Price Stability

Rates are completely locked at purchase for up to 30 years.

Scales upward predictably as you cross into higher age brackets.

Medical Underwriting

Full evaluation locks in low rates for young, healthy parents.

No medical exam required; pricing is averaged across the pool risk.

Coverage Capacity Caps

Can scale to multi-million dollar limits tailored to your debts.

Strictly capped, frequently at 1x or 2x your gross annual salary.

Beneficiary Discretion

Complete control over assignments and trust structures.

Limited structures managed through corporate administrative rules.

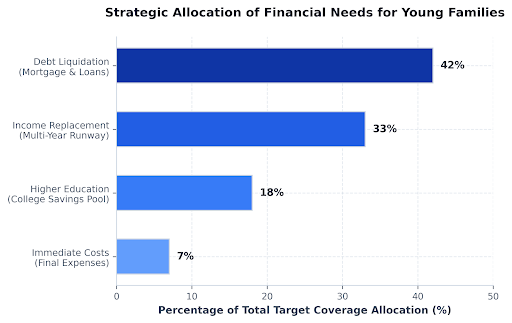

Visualizing Capital Allocation Priorities

To understand how a life insurance payout functions, you must view it as a direct replacement for your lifetime earning capacity. The following chart illustrates how a balanced, family-centric protection plan distributes capital to isolate dependents from long term financial stress.

Building a Personalized Target via the DIME Method

When determining how much coverage to buy, young parents should move past simple multiples of income and build an accurate calculation using the DIME Framework. This model breaks your family’s future liabilities down into four concrete categories:

1. Debt Liquidation (D)

Sum every dollar of immediate consumer liability your household carries. This baseline must include student loans, auto financing, credit card balances, and personal lines of credit. Clearing these high interest obligations immediately reduces your family’s monthly cost of living.

2. Income Replacement (I)

Calculate the true net cash flow required to support your family over an extended timeline. A dependable guideline for young parents is to multiply your current net take home salary by the number of years remaining until your youngest child graduates from university or reaches full adulthood.

3. Mortgage Elimination (M)

Factor in the complete remaining principal balance on your home loan. Allocating capital to fully pay off the mortgage guarantees that your family secures their housing stability, freeing them from the burden of monthly housing payments during a difficult transition.

4. Education Funding (E)

Project the future cost of higher education for your children. With university tuition trends increasing steadily, setting up a dedicated capital pool for tuition, housing, and instructional supplies prevents your children from needing to take on substantial student loan debt.

Subtracting your active liquid savings, current investments, and existing individual policies from this global total reveals your true target coverage amount. This ensures you buy exactly what your family needs without overpaying for unnecessary coverage.

Navigating Product Structures: Term vs. Permanent Coverage

Once you have calculated your target coverage amount, you must select the most efficient product structure for your household budget. The market is broadly divided into two product philosophies:

Term Life Insurance: Pure, Targeted Risk Management

Term life insurance provides straightforward death benefit protection for a specific window of time, typically 10, 15, 20, or 30 years. For young parents, a 30-year term policy is highly effective. It covers the exact decades where your financial liabilities peak: while your mortgage balance is high and your children are entirely dependent on your income.

Because term policies include no complex internal investment mechanisms or cash value features, they are exceptionally cost-effective. A healthy 28-year-old can easily secure a $1,000,000 policy for less than the cost of a standard streaming service subscription, allowing you to maximize protection without straining your monthly savings goals.

Permanent Life Insurance: Lifelong Bundled Assets

Permanent insurance policies, such as whole life or universal life, provide lifelong coverage and include an internal cash value savings component that grows over time. While this cash accumulation feature can be useful for high-net-worth estate planning or managing complex tax strategies, permanent premiums can be 5 to 10 times more expensive than equivalent term policies.

For the vast majority of growing families, dedicating substantial capital to high permanent premiums can lead to structural underinsurance, where parents purchase smaller policies than they actually need to save on costs. An efficient path for standard wealth building is to buy affordable term insurance to lock in full protection and independently invest your premium savings into diversified, low-cost tax-advantaged retirement accounts.

Step-by-Step Security Timeline for Young Parents

To transition from planning to execution seamlessly, follow this definitive protection strategy:

Step 1: Conduct a Comprehensive Liability Inventory

Gather your household financial documents. Note your exact remaining mortgage principal, outstanding consumer debts, and baseline monthly living expenses. Track your children’s current ages to determine your income-replacement timeline.

Step 2: Test Variations via an Interactive Planning Model

Run your numbers through an online calculator to evaluate different financial coverage scenarios. Always round your final coverage target upward to build in a reliable buffer for future cost of living shifts and unexpected medical expenses.

Young Parents Life Insurance Calculator

Systematically estimate your household’s true coverage target by mapping your children’s development timelines.

1. Household Profile Inputs

Credit cards, student loans, auto loans, personal financing

Your annual net earnings to replace for the household

The runway scales automatically to replace income until age 22.

Total outstanding balance required to pay off home loans

Allocated college savings pool target for tuition/housing

Savings accounts, active investments, existing individual coverage

2. Calculated Coverage Target

Net Target Life Insurance Need

$0

DIME Component Allocation Bar

(D) Consumer Debt Clearing

$0

(I) Income Replacement (20 Yrs)

$0

(M) Mortgage Elimination

$0

(E) Total College Funding

$0

Less: Existing Assets Offset

-$0

Processing financial parameters…

Step 3: Work with an Independent Insurance Broker

Avoid applying directly to a single captive insurance carrier. Captive agents can only sell policies from their specific company, whereas different insurers use completely different guidelines to price risk. An independent insurance broker can shop your profile across dozens of competing carriers, matching your family’s profile with the company offering the lowest long-term premium rates.

Summary and Next Steps

Protecting your family’s financial future requires moving past generic assumptions and building a plan based on your household’s actual liabilities. By systematically tracking your debts, income replacement timelines, mortgage balances, and education targets, you can secure an affordable policy that keeps your dependents safe.

Locking in an independent individual term policy while you are young and healthy allows you to establish a stable financial foundation at the lowest possible cost, providing true long term peace of mind for your loved ones.